I'm Going to Work Until I Die

I

talk a lot about Baby Boomers, but The Greatest Generation was a real, “pull yourself up by the bootstraps” kind of crowd. They faced several unique retirement challenges during the Great Depression, and many of them pioneered the “do-it-yourself” attitude of retirement. When you think about it, retirement planning is a fairly young concept, so it’s no wonder future generations will reform current concepts like the traditional three-legged stool and the 60/40 portfolio. Unfortunately, many Baby Boomers still believe their plan is to, “Work until I die,” like their predecessors once did. Look, any plan is better than no plan, but working forever isn’t a plan. Let me show you how recent research suggests that this do-it-yourself plan is becoming more popular, but I’ll also show you why it is suboptimal.

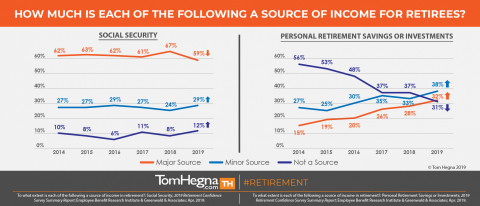

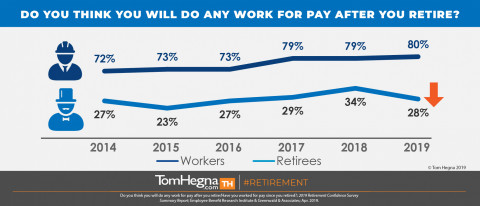

In a previous article, I cited the Employee Benefit Research Institute’s (EBRI) annual Retirement Confidence Survey (RCS). They research current workers approaching retirement and recent retirees side-by-side, and the 2019 research continues to show a paradigm shift. The data suggests that retirees are relying less on Social Security but more on personal savings and investments. Furthermore, “Three in four workers expect their personal savings or investments to be a source of income in retirement,” and, “Four in five workers expect to work for pay after retiring.” However, there are some flaws in this plan.

While a significant number of current workers plan to “work for pay” in retirement, retirees show the actual result of this plan. Only three in ten retirees actually have worked for pay since retiring. Plus, four in ten retired earlier than planned, and 35% did so due to a health problem or disability, which was probably a major reason their “work for pay” plan failed. There were several other reasons reported for retiring earlier, but that just goes to show the volatility in a “work until I die” plan. How can someone enjoy retirement without knowing they have some stability in their plan? Retirement planning is all about managing risks, and any plan that doesn’t include guarantees will be less than it could have, would have, or should have been!

I’m not saying that you shouldn’t work in retirement. I’m just saying it shouldn’t be the foundation for your plan. Start your plan by developing a budget so you can see the basic expenses you’ll need to cover. Then look at sources of guaranteed income you can never outlive, and use them to cover those basic expenses. The bottom line is, working for pay isn’t guaranteed lifetime income. Don’t use it to cover basic expenses. Jobs can be lost, businesses can close, and we all become more injury-prone as we age. Including guarantees is what creates a worry-free retirement so you can actually ENJOY it! And remember, only an insurance company can manufacture mortality credits that reward you for living longer. That’s like getting paid WITHOUT having to work! One advisor calls these credits “other people’s money.” He says, “You don’t have enough money on your own to retire right now, but I can find you some other people’s money…”

See you after work,

Tom Hegna